FX Periscope INR Overvaluation Getting Stretched Webinar

- First Basis

- Aug 13, 2024

- 7 min read

Venkatesh Bijoor, sir, CSO and co-founder, First Basis As the Chief Strategy Officer in the webinar are assisting, and learning more about Quantico, when Venkatesh Sir is speaking, he will tell. Why is FX Periscope? We have been discussing it with Dr. Shubhada Rao, Yashvardhan Rao, and those of us and his friend Yuika . There is a lack of combined technical and fundamental reports, basically focusing on rupees. As a result, banks release various reports. If they come out with fundamental reports, the technical reports are missing. Here at the FX Periscope, an effort is made to combine the technical as well as the fundamental reports. Most of the articles are contributed by Quantico, Vivek, and Yuvika. They are well versed in the financial markets. What is happening in the rupee? What are the financial markets? Having worked in the bank, they are well versed in the rupee market and a bit of technicals as well. And in the case of Yashvardhan Rao, he has been a veteran in this report as a trader and as a consultant in currencies as well as commodities. He writes technical reports. So he writes technical as well as commodities. He writes technical reports. So he writes technical reports. He is well versed in the fundamentals, too. We make an effort to connect the fundamental and technical analyses in the report. That is what we are trying to do. do. And we already have 6 or 7 periscope reports.

For all of you who are participating today, if you leave your email ID, we will share with you a few old reports and one complimentary report for August. With this background, let me give you a brief introduction to Yashvardhan Rao and Mr. Vivek, who joined Quantico Research in November 2020. He holds a master's degree in economics from the Delhi School of Economics and brings close to 18 years of rich industry experience in the field of macroeconomics research with a focus on financial markets, especially currency, fixed income, and money markets. He has extensive experience engaging Treasury clients, foreign investors, regulators, trade associations, and multilateral bodies over coverage of the economic and market outlook for India. Basically, I have told you that he can be called a specialist in Indian rupees on fundamentals. Over the last decade, Vivek has also been addressing key industry associations. His views on the Indian economy are widely covered in the media, including financial media houses. He regularly writes in-depth columns for media publications. His views on markets are keenly followed by Treasury teams in corporations and banks. Prior to joining Quantico, Vivek worked as a president and senior economist at S Bank. His earliest stint included the roles of Treasury economist at ICIC Bank and Research Associate. And about Mr. Yashvardhan Rao, he has been a dealer in foreign exchange since maybe 1985. He started his career at the Indian Overseas Bank. As a chief dealer there, he left and joined a consulting firm. From there, he joined Arvind Mills as head of the Treasury.

He worked at Arvind Mills as head of Treasury for over 10 years, and he is a keen technical analyst. He studied himself, and more on that he will himself share. will himself share himself will share. Will himself will share when he was charting and all there was no software, like whatever was available, it's all done in books. You know, that is from his beginning, and he has interacted with various authorities, you know, various people who are today celebrities in technical analysis. From Arvin Mill, he moved to Reliance in the commodity section, and he advised them in commodity oils and various commodities for over 10 years. He has been an advisor to FX First Basis and a consultant to us for the last 10 to 12 years. He has a keen interest, and his technical reports are the most sought-after in the market. I am sure I am using them for hedging decisions, and my clients are happy with that because we are making money out of them. With this brief introduction of Rao, I will request that Mr. Vivek share his opinion about the Vivek sir, explain to us the importance of regrading FX Perscops. He explains some of the targets in the market the market in the last two years, considering the fact the fact that we achieved in the market the market last two years GDP increase by like sector Road, Raliways and housing all this factors arepervilling Macroscopev visiblite Fythe government are Fy is no 4.4 % but next year physical defination target the Government FY traget should be 4.5% We We are easily covering half of FY25 in compression. compression. He explains

Is the budget inflationary?

The Union The Union Budget FY25 is not inflationary; there were no populist policies, e.g., no direct income transfer, transfer, etc., announced. Moreover, the quality of financial spending continues to remain healthy.However, inflation continues to remain a headline. headline. CPI inflation rose to a 4-month high of 5.08% in June–24. June 24 vs. . 4.80 on May 24.Food inflation continued to add upside pressure, with the RBI in its monthly bulletin calling recent inflation experience over the last year not transitory in nature any longer.

Monsoon: An uneven story

Southwest monsoon rainfall, after remaining in deficit through much of July–24, has now moved into a surplus, at 7$ of LPA as of August 6–24. Nevertheless, the geographical distribution remains highly uneven.The exposure of kicking in La Nina has been pushed to August 24 by international agencies.Although karif sowing has produced satisfactory prograss so far, the price of perishables, especially potao, tomato, and onion, is yet to moderate in a convincing manner.

Funding of the fiscal deficit

FY25 gross and net market borrowing have been budgeted at Rs 4.01 trillion and Rs 11.63 trillion, respectively. Net market borrowing is expected to finance ~69% of the FY25 fiscal deficit, down from ~37% in FY24.Total gross borrowing by the central government and PSEs is budgeted to moderate to 4.5% of GDP in FY25, down from 5.4% in FY This is now getting close to the per-COVID threshold of 4.6%.

The interest rate is moderate

The faster pace of fiscal consolidation will be viewed favorably by the RBI ads. It will help to curb pressure on CPI inflation, with CPI inflation expected to moderate to 4.5% in FY25 from 5.4% in FY25. We expect the RBI to start easing monetary policy in Q3 FY25, with a cumulative rate easing of 50 bps in FY25.We continue to expect the 10-year g-see yield to drift lower to 6.75% by March 25, as FPI bet flow is likely to be supportive amidst India's index inclusion.Impact of fiscal deficit on INR: The INR shows a low-to-moderate relationship with the fiscal deficit. The macro-asset tends to strengthen when the fiscal deficit is either significantly lower or higher than the long-term historical average of~5% of GDP. From a FY25 perspective, the tragic fiscal deficit of 4.9% is close to the long-term average; this probably would blunt the chances of any extreme movement in INR.

INR: The current context

The INR continues to stay in a prolonged phase of stability despite signs of volatility in the global FX market. Expectations with respect to the commencement of monetary policy easing by the US Fed have strengthened over the last month. Market participants are pricing in three rate cuts from the US Fed before the end of 2024. This is unlikely to provide a major headwind for the USD, as the Fed is a late entrant to the monetary easing camp.

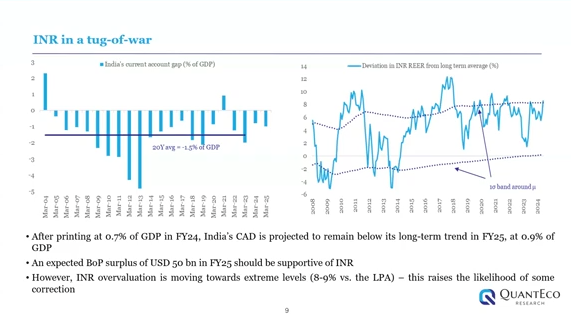

INR in a tug of war:

The After printing at 0.7% GDP in FY24, India's CAD is projected to remain below its long-term target in FY25 at 0.9% of GDP. An expected BoP surplus of USD 50 bin FY25 should be supportive of INR. However, the INR overvaluation is moving to an extreme level of 8–9% compared to the LPA. This raises the likelihood of some correction.

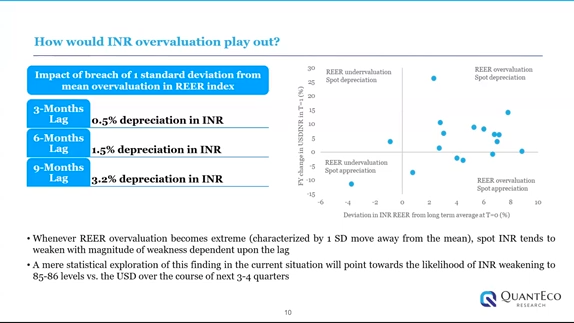

How would INR overvaluation play out?

Where REER overvaluation becomes extreme, characterized by a 1 SD move away from the mean, spot INR tends to waken with the magnitude of weakness depending on the angle of the leg. A mere statistical exploration of this finding in the current situation will point to the likelihood of the INR weakening to 85–86 levels vs. the USD over the course of the next 3–4 quarters.

INR Outlook

We expect the RBI to continue to display a bais for reserve accumulation to fortify country impact coverage, which on a FCA basis currently stands between 9 and 10 months.We expect the rupee to post a mild depreciation in FY25, with USDINR expected to drift higher towards 84.5 levels by the end of March-25. The market consensus is mildly bullish on INR, with a year-end expectation of 82.8. Geopolitical uncertainty and delays in the Fed pivot could pose a risk to our view.

Fx Periscope, an indispensable companion to the Treasury September Saliebt Features

It gives valuable views monthly on most of the popular currencies in Paris.The views given are mostly definite and do not leave anything to doubt.All the points covering the direction, the entry levels, the objective, and the risk levels are discussed in a concise manner without leaving much room for doubt.Even though the views appear purely technical, they are in fact written, considering macro pictures are also in the background, making it a sort of hybrid analysis.

Frequently Asked Questions

How does a Treasury Management System contribute to operational efficiency?

By automating routine treasury tasks such as payments, reconciliations, and reporting, a Treasury Management System reduces manual errors, saves time, and enhances overall operational efficiency.

What Is Online Market Research

Online market research uses the same strategies and techniques as traditional primary and secondary market research, but it is conducted on the Internet. Potential customers may be asked to participate in a survey or give feedback on a product. The responses may help the researchers create a profile of the likely customer for a new product.

Why Should You Invest?

So why wait? Investing in strategic planning and management consulting can be the key to taking your business to the next level. Don’t let your competition get ahead and take control of your future today. By investing in these services, you can ensure that your business is running as efficiently and effectively as possible, positioning yourself for long-term success.

How do management consultants help in risk management?

They analyze potential risks, develop mitigation strategies, and help implement robust risk management frameworks to safeguard the organization’s assets and reputation.

How can market research minimize business risks?

By providing accurate and up-to-date information, market research helps businesses anticipate market changes, avoid potential pitfalls, and make informed decisions to mitigate risks.

Comments